By Paul McIntyre & Brendan Coyne

This article first appeared on marketing website Mi-3

Woolworth's-owned Cartology might have made the early running in building its $300m supermarket media unit in a category with commercial potential of $1bn but the broader "owned" media sector - media assets owned by brands including websites, apps, email and stores - is four times bigger than grocery and liquor at $3.9bn, according to a new benchmark report from media valuation firm Sonder. "Aggregated’ retail" - think Officeworks, Big W, Myer and JB Hi-Fi - is a bigger prize than supermarkets and Sonder's calculations of owned-media margins in the 80-90 per cent range are turning CEO and CFO heads. That could alter the balance of power between marketing, sales and merchandise, and potentially change the dynamics between paid, owned and earned investment. Sonder founders Jonathan Hopkins and Angus Frazer run the rule over five standout categories – grocery and liquor, aggregated retail, telco, petrol and convenience, and finance – and identify which players may be next to market (hint, anyone with a loyalty programme) and the implications for Australian media market dynamics.

What you need to know:

New report suggests Australia’s owned media potential, at circa $3.9bn, dwarfs retailer media – and is far broader than selling space to suppliers.

Telco, banks and finance, petrol and convenience and travel categories have almost $1.5bn in owned media potential and category leaders are unlocking it to drive growth, improve CX, prove ROI from loyalty programmes – and reduce reliance on paid media.

Meanwhile, within retail, the push for “80-90 per cent margins” on media is changing the competitive tension between merchandise and marketing, with owned media sitting squarely in marketing’s domain.

In the main, email “contributes the most revenue of all digital channels”, per report co-author and Sonder co-founder Jonathan Hopkins. “Email is the sleeping giant of owned media and we value it extremely highly.”

But in-store media has major growth potential across verticals including telco and petrol-convenience.

Report outlines the main owned media players across categories, which brands and retailers have the most immediate potential to become market leaders, and what the next growth wave may mean for market dynamics.

Listen here for the full analysis on Mi3's podcast with Jonathan Hopkins and Angus Frazer.

“We expect the retail media explosion to continue. There's a long list of challengers to the top five as they start to get their act together, value what they have and then work out how to leverage it.”

— Jonathan Hopkins, founding partner, Sonder

All the noise of late has been around retailer media with Cartology making the early running and Coles imminently joining the billion-dollar fray. But owned media is much bigger – estimated at $3.9bn in total in Australia – and there are dozens of players coming up on the inside rail across telcos, banks, service stations, travel and utilities as well as high street department stores or ‘aggregated’ retail. Much of the value is within bricks and mortar stores – where Sonder forecasts a greater build out of in-store media – as well as within unsexy channels like email, “the sleeping giant of owned media,” per founding partner Jonathan Hopkins. Display and search, according to the firm’s new report, is only about 10 per cent of the pie when it comes to owned media potential.

Across the piste, Hopkins thinks there is huge upside for owned media growth. Operators that start to “behave like a media owner” and go beyond cannibalising trade budgets and flogging media space, can “generate massive step change in revenue.”

If firms can better value and articulate that value to new and existing suppliers, Hopkins thinks there is also an opportunity for marketing departments to create a less combative dynamic with merchandising and sales teams, potentially shifting the balance of power. “It tends to be the marketing department [that gets control of owned media],” says Hopkins. “All roads tend to lead to them”.

Numbers game: where did they get $3.9bn from?

Defining owned media’s value is no mean feat. Whereas paid media is reported and earned impressions can be quantified in terms of media cost equivalents, owned media – the value of the media assets and channels that brands own or control like email, apps, e-commerce, websites, catalogues and retail stores – is more nebulous.

But Sonder has had a crack, “ranking businesses that are leveraging their owned media ecosystem in some way commercially”, according to Hopkins. I.e. not necessarily directly leveraging those media channels for ads or third party comms (though sectors such as retail and grocery definitely are taking that approach) but also where they are generating indirect revenue. “For example with sponsorship partners within loyalty reward programmes, which is common within telco and finance”, says Hopkins, citing Amex as a standout example.

“So the numbers in the report refer to the commercial potential – which is the maximum potential that a business could procure from leveraging their own media.”

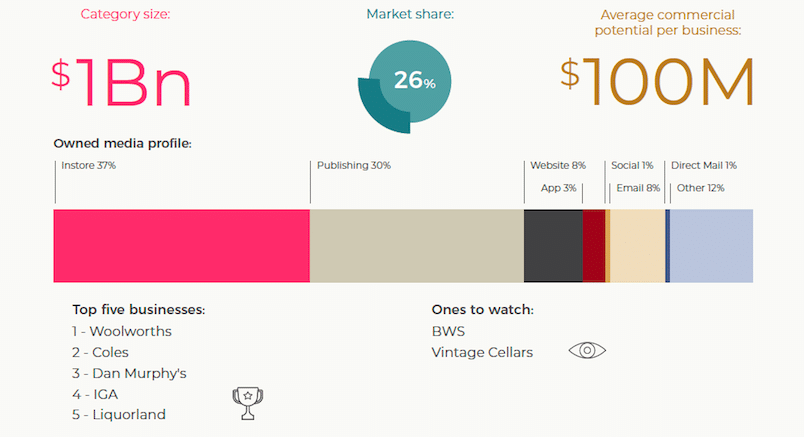

Grocery & liquor category value, main players, ones to watch and media channels doing the lifting. Pic: Sonder

Grocery and liquor: $1bn

On that basis, the firm calculates grocery and liquor, “the poster child for owned media leverage”, has current potential value of $1bn. First mover, Woolworth’s-owned Cartology is top of the pile.

“They remain the biggest and most sophisticated owned media business in the country – some might say beyond that as well,” says Hopkins.

“They take in the smarts from established players in the US and Europe and then having Woolies X and Quantium reshaping their everyday rewards data to attract advertisers is crucial to their success. And that data-led media solution model is something that others are starting to replicate.”

Coles is now bidding to catch up. “They haven't quite hit their stride yet, but they're very powerful - media platforms in the shape of magazine and radio and their store network, so they will provide a threat,” per Hopkins.

BWS and Dan Murphy “were already in strong positions but just got stronger” with Endeavour Group last month launching its media business MixIn. Metcash-IGA is another emerging player while Sonder reckons Liquorland and Vintage Cellars are also ones to watch.

Don't put cart before horse

The challenge is not fracturing existing relationships with suppliers by squeezing them too hard for media dollars.

“The supermarkets have been careful not to upset the apple cart,” says Hopkins.

“Their merchandise teams are typically the custodians of supplier relationships and it would be foolhardy to upset that ... So it's all about educating the merchandise team on the value of media, understanding what they're leveraging and how to leverage it – and working in tandem with the sales team and the marketing team, depending on the model that the business adopts,” he adds.

“That may involve one briefing with the trade marketing team and the brand marketing team briefing the host business together, which can work. Or it may be about dividing and conquering, keeping things church and state and carving off media for a sales team to sell and giving the merchandise team an amount of inventory to leverage as well,” says Hopkins.

“There are different models that can work.”

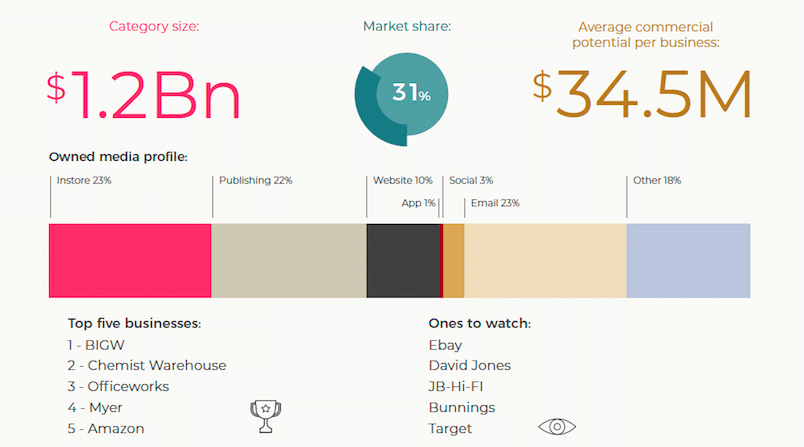

Retail aggregator main players, ones to watch, size of the prize and channels at work. Pic: Sonder

Retail aggregators: $1.2bn

Chemist Warehouse, Officeworks, Myer – plus Woolworths-owned Big W – make up four of the top five retail aggregators, alongside Amazon, which last year made $63m from media locally. But others with potential are David Jones, JB Hi-Fi and Bunnings, “which could easily break into the top five” of an owned media category that Sonder calculates currently holds $1.2bn in potential value. While the firm suggests The Iconic has ‘strategic capability’, the likes of JB Sports and Supercheap Auto are listed as ones to watch in the shorter term.

“We expect the retail media explosion to continue. There's a long list of challengers to this top five as they start to get their act together, value what they have and then work out how to leverage it. David Jones has had a good store refurbishment with multiple digital screens. They've got a breadth of vendors to sell to and a highly desirable customer base, so they're well primed," says Hopkins.

"JB Hi-Fi has potential to extract more revenue from the market by expanding their leverage to align with those more advanced retailers. Bunnings has been fairly conservative, because they're doing so well as a business. But we think they could easily jump into that top five by making more of their media available to market,” he adds.

“Target is another potential player. They were quite pioneering in the US, creating a sales business called Roundel, so they have the capacity globally and could be one to watch in Australia as well,” Hopkins suggests.

“It tends to be the marketing department {that gets control of owned media}. They work in collaboration with merchandise and sales and category managers. But because the marketing department owns the channels, then all roads tend to lead to them.”

— Jonathan Hopkins, founding partner, Sonder

Merchandise versus marketing: Retail power shift?

Wringing maximum value from retailer owned media requires businesses to set up with customer experience at the fore, feeding back the data and ultimately better valuing owned media, instead of throwing it to suppliers as a value-add, according to Hopkins and Frazer.

While early days, they think that shift is underway, given the “80-90 per cent” margins to be made. As the market matures, the dynamic between merchandise and sales teams and other parts of the business could be altered. Properly valuing owned media could swing the pendulum of power back towards marketing – which has historically battled merchandise for influence, particularly within the large supermarkets.

“Compared to the US, Australian retailers have been relatively slow to develop their owned media sales offerings. But in the last 12 months, we’ve seen that shift, with merchandise teams either understanding the value of what they’ve been leveraging, or senior folks within the business saying, ‘this is something we’re going to go after, make it happen’. And once you see the numbers, they’re so compelling that it’s a bit of a no brainer,” says Hopkins.

“It tends to be the marketing department [that gets control of owned media],” he adds. “They work in collaboration with merchandise and sales and category managers. But because the marketing department owns the channels, then all roads tend to lead to them – they want to manage sensitively their own communications with customers as well as partner communications. It makes sense for it to land there.”

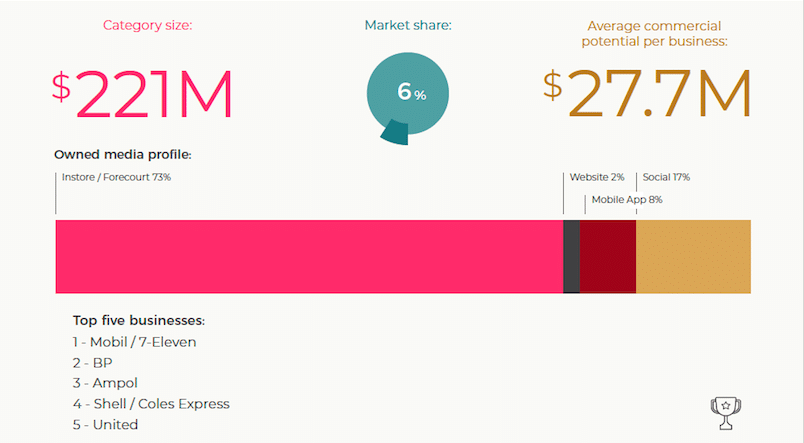

Petrol & convenience: Forecourt and in-store media make up vast bulk of revenue potential. Pic: Sonder

Petrol and convenience: $221m

The firm’s report pegs petro-convenience ($221m) as another significant opportunity for owned media leverage with Mobile/7-Eleven, BP, Ampol, Shell/Coles Express and United the top five firms ranked. Across the category, there’s potential for circa $30m in revenue per operator with in-store media adding to existing pump/forecourt screens.

“I think where we’ll see some growth will be around in-store experience because historically, that hasn’t been great,” says Sonder founding partner Angus Frazer. “What we’re seeing is more of these businesses creating cleaner store environments, reducing clutter and focusing on the really high value media within the store. In doing that, you’re improving the customer experience and you’re still maintaining a focus on the owned media channels that really add value.”

The sector has undergone significant structural change of late, with Coles offloading its business last month to Viva Energy, following Woolworths, which exited in 2018, and Caltex’s rebrand to Ampol. The deals may lead to strategic shifts, but Frazer thinks there is room for hybrid models, with the likes of VMO operating a sizeable screen network: “Being able to outsource media sales when it comes to forecourt media, while being able to commercially leverage your in store and ambient media, could be a really interesting model.”

Travel, telco, banks: $900m-plus

Banks and finance ($152m), telco ($255m) and travel ($488m) are already leveraging significant scale to collectively nudge a billion dollars.

But more than half of that is made up by a “mature” travel sector via Qantas and Virgin leveraging data and tapping partners across inflight entertainment, boarding passes, luggage, carousel, posters, itineraries, apps, loyalty programs, emails and websites, with dedicated sales teams, internal and external, notching up media margins of circa 90 per cent versus 3 per cent on flights.

Hotels though have some headroom for growth with Intercontinental Hotels Group tipped as the one to watch.

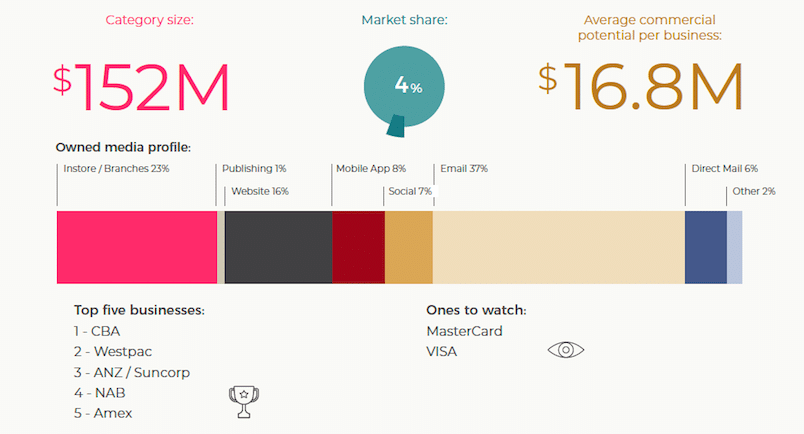

Commbank tops owned media potential within finance, though other banks are closing the gap. Credit card providers are also delivering big results for merchant partners via loyalty programmes Pic: Sonder

Finance: Commbank leading for now

Of the banks, Commbank is in the lead, “but the likes of ANZ, Westpac, NAB are all right there as well,” says Frazer. “While the commercial potential isn’t as high as some other categories, it’s the strategic potential which is really interesting for them: We’ve seen a very strategic use of their own media – starting with owned media first, getting those communications optimised before you go into paid media – we’re seeing the banks do that really well.”

Though not selling media inventory, the banks are using it to cross-sell services with Commbank pushing its owned or part-owned investments – such as retail marketplace Little Birdie or DTC mortgage platform Unloan – through its app and ‘Yello’ loyalty programme, and ANZ bringing retailers and brands into play via its partnership with Cashrewards.

“When you combine these large databases that they have through rewards programs with the data that they have on people, you’ve got this incredibly powerful opportunity for the banking and finance sector,” says Frazer.

He thinks Amex is another one to watch, given the strength of its merchant offers programme.

“Because Amex have the downstream financial data. They understand what their customers and members are actually doing and how they’re responding to merchant offers. So the media value that is being provided in there is being leveraged through commercial terms primarily, and it’s about using that media value to attract more and higher value offers for the card members,” says Frazer.

“So there’s this win-win whereby the card member has a better experience – they are getting better offers from more brands. The merchants are able to provide these offers and they’re seeing where the value is coming from and the performance. So we’re seeing a lot of [owned media] growth in reward and loyalty type programmes.”

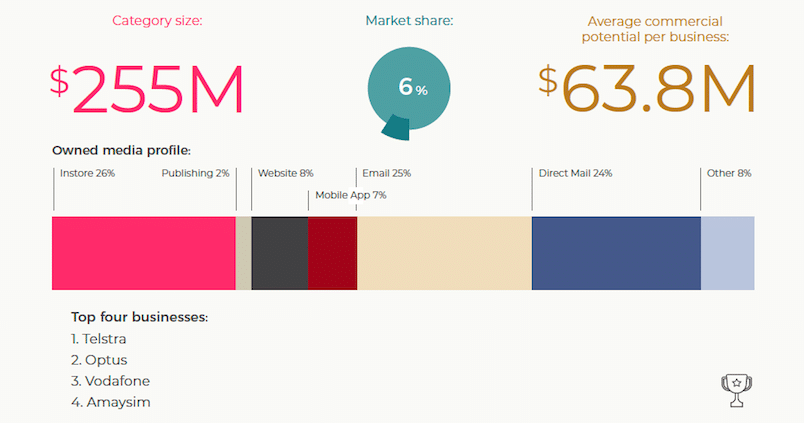

In-store, email and direct mail are major channels for telcos aiming to leverage owned media. But in-store could be the next growth driver. Pic: Sonder

Telco: “very, very powerful”

Telcos Optus and Telstra are already operating media businesses, but less than a third of the media telcos own is being commercialised – and there’s a lot more the category could do, reckons Frazer.

“Optus has sports content, which is Optus behaving like a traditional media owner and securing very lucrative content deals. Telstra has also long monetised owned media; they have a JCDecaux partnership looking at monetising payphone screens and at a more strategic level, their investments in Foxtel,” he says. “These businesses, whilst there are only a few, are very, very powerful.”

Frazer thinks the next growth frontier is physical media as customers come into stores to try new tech. “Having a strong in store presence is really important and having the media to back that up is critical – and these are really powerful media assets that other brands want to be able to tap into as well.”